Categories

Investment, Investment Property, Multifamily properties, Rental properties

If you're trying to figure out how to invest in multifamily in Miami without losing sleep — and without buying a syndicator's pitch deck — this is the roadmap I give my own clients. I've spent 11 years walking duplexes in Coral Gables, triplexes in Little Haiti, and fourplexes in Allapattah. I've seen which deals print cash and which ones quietly bleed their owners. Miami multifamily can be one of the cleanest investments in the country, but only if you respect a few rules that most online guides skip. Let's get into the actual mechanics.

Why Multifamily Beats Condos as a Miami Investment

I've written separately about why I steer most investors away from condos, but here's the short version: with a small multifamily property, you own the structure and the land. No HOA. No board. No risk of a $40,000 special assessment landing in your mailbox after a SIRS reserve study. You collect 2–4 rent checks per closing, and you control the asset.

A condo can make money. Multifamily, for an investor-only goal, almost always makes more.

The "Four or Fewer" Rule — Stay Under the Commercial Line

I want every first-time Miami multifamily investor to stay at four units or fewer. Two reasons.

First, 2–4 units still qualify for residential financing — conventional, FHA owner-occupied, or DSCR. Once you cross to five units, you're in commercial loan territory: shorter amortizations, higher rates, stricter underwriting. ( Anibal Torres at CMG Home Loans broke down the recent Fannie Mae multi-unit financing changes if you want the technical detail on what counts as residential.)

Second, with four or fewer units you can usually self-manage. Property management fees in Miami run 8–10% of gross rents. On a $5,000/month duplex, that's $5,000–$6,000 a year — gone. Skip the PM, do the work yourself, and that fee becomes cash flow.

Bigger Units Beat More Units — The Turnover Math

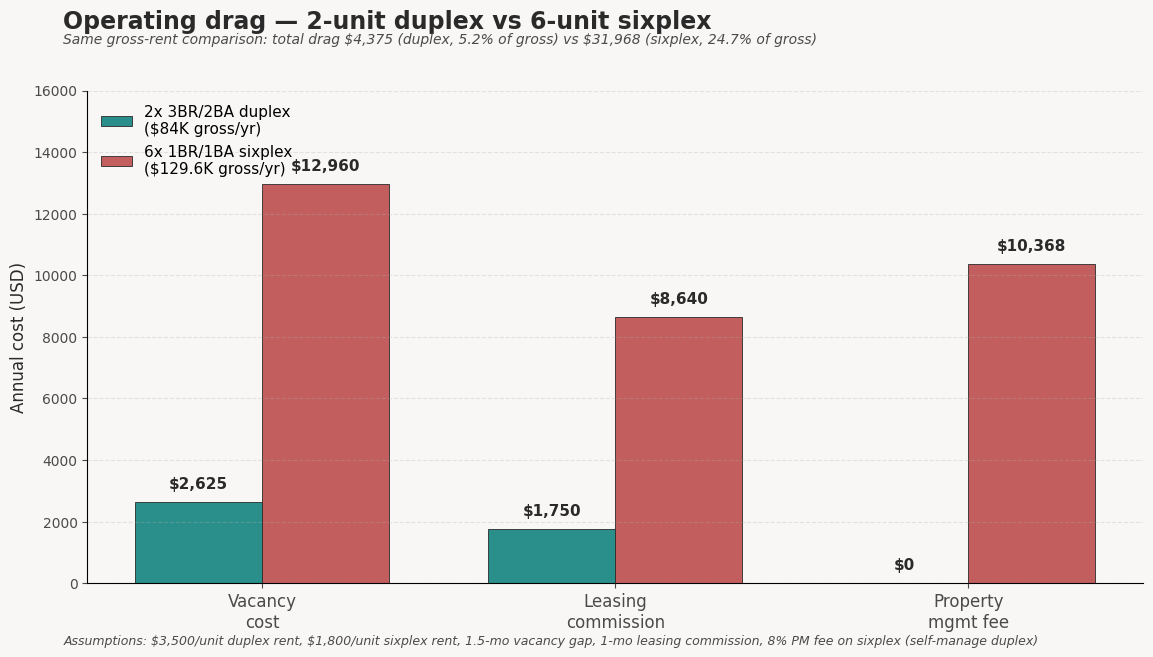

This is the single most ignored rule in Miami small multifamily investing. A duplex with two 3BR/2BA units will out-perform a sixplex of 1BR/1BA studios almost every time. Why? Turnover.

Studios and 1-bedrooms turn over every 12–18 months. Families in 3-bedrooms stay 3–6 years. Every turnover costs you:

- 1–2 months vacancy

- Leasing commission (often 50–100% of one month's rent)

- Make-ready paint, cleaning, small repairs

- The risk of a worse tenant on the next lease

Multiply that across six small units and you're refilling 4–5 leases a year. Across two big units you're refilling one every 3–4 years. That delta lands directly in your cash flow.

Assumptions for the comparison below (realistic 2026 Miami rents, middle-Miami submarket):

- Duplex: 2 units × 3BR/2BA at $3,500/mo each = $7,000/mo gross = $84,000/yr

- Sixplex: 6 units × 1BR/1BA at $1,800/mo each = $10,800/mo gross = $129,600/yr

- Per-turnover cost assumptions are identical in both columns: 1.5 months vacancy gap + 1 month leasing commission. Per-turnover cost is the same whether the tenant stayed 1 year or 5 — what changes is frequency , which is why long tenancy wins.

| Scenario | 2× 3BR/2BA duplex | 6× 1BR/1BA sixplex |

|---|---|---|

| Per-unit rent | $3,500/mo | $1,800/mo |

| Gross annual rent | $84,000 | $129,600 |

| Avg tenant tenure | 3–6 years (4 yr midpoint) | 12–18 mo (1.25 yr midpoint) |

| Annual turnovers | 0.5 (2 units ÷ 4 yr) | 4.8 (6 units ÷ 1.25 yr) |

| Vacancy cost (1.5 mo × rent × turnovers) | $2,625 | $12,960 |

| Leasing commission (1 mo × rent × turnovers) | $1,750 | $8,640 |

| Property mgmt fee (8% of gross) | $0 — self-manage | $10,368 |

| Total drag on gross income | $4,375 | $31,968 |

| Drag as % of gross | 5.2% | 24.7% |

The sixplex looks better on the surface — $129K gross vs $84K. But operating drag eats a quarter of it. The duplex keeps 95% of its top line because turnover is rare, the units are big enough to attract families, and you don't need a property manager. That gap is the entire investment thesis.

Buy Newer If You Can — Why Year Built Decides Your Cash Flow

Brand new is best. Five years old is good. Ten years old is still acceptable. After that, Miami's environment starts to bite back.

Florida insurance carriers penalize older buildings hard — South Florida HO premiums currently run $4,375–$7,290+ per year and the oldest housing stock pays the most . A 1955 frame duplex with the original roof and 60-amp panel can be uninsurable through standard carriers. You end up on Citizens or in surplus lines, paying double.

Beyond insurance, newer buildings give you:

- A roof with 15–20 years of life left (a Miami roof replacement is $20K–$45K)

- Modern AC and impact windows (insurance discount)

- Higher market rent — tenants always pick the newer building when rents are similar

This is why I push my Miami multifamily clients toward post-2010 builds whenever the budget allows. A new duplex at $850K often out-cash-flows a 1955 duplex at $625K once you load in insurance and capex.

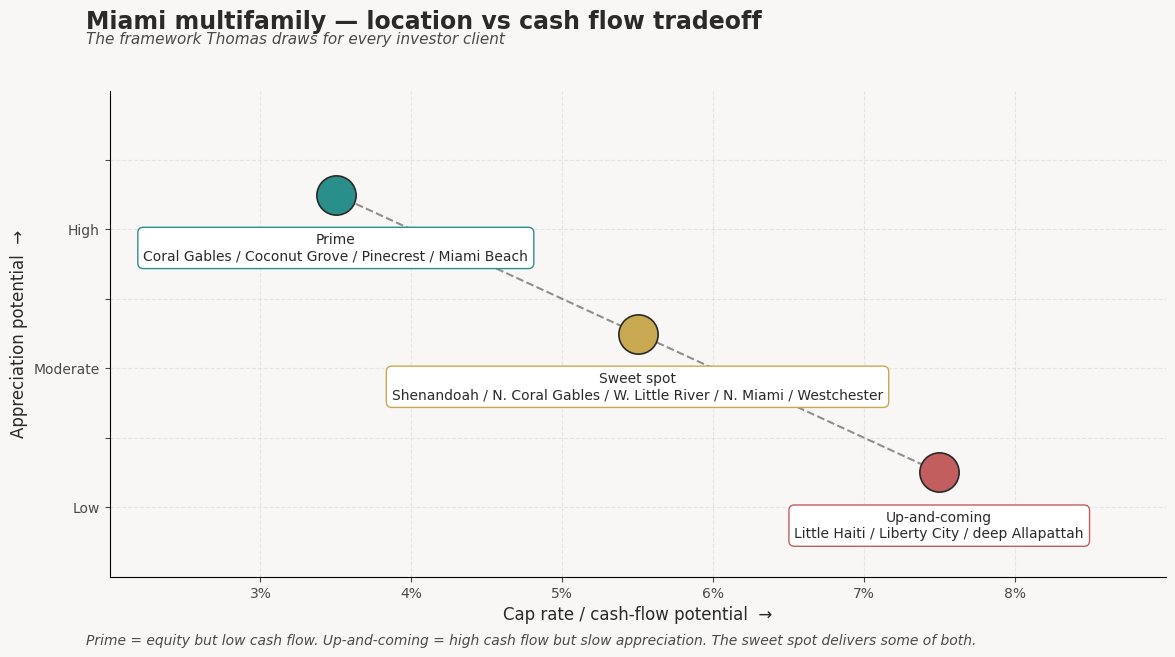

Location vs Cash Flow — The Miami Tradeoff

This is the framework I draw on a napkin for every investor I meet. There are three zones in Miami-Dade:

1. Up-and-coming areas (parts of Little Haiti, Liberty City, deep Allapattah, Brownsville). Higher cap rates — sometimes 7–9%. Best raw cash flow. But: more deferred maintenance on the building stock, longer rehab timelines, slower appreciation, and more hands-on day-to-day management. Best for investors who want to be active operators, not passive owners.

2. Prime locations (Coral Gables, Coconut Grove, Pinecrest, parts of Miami Beach). Strong equity build, top-shelf tenants. But: rents rarely cover the debt service at today's prices. Cash flow gets crushed; you're playing for appreciation.

3. The sweet spot — middle Miami (parts of Shenandoah, North Coral Gables, West Little River, North Miami, Westchester). Decent appreciation and survivable cash flow. This is where I point most clients.

Prime location = equity but low cash flow. Up-and-coming = higher returns but slower appreciation. The middle is where most investors should buy.

Pick your zone based on what you actually need from the deal — passive income, equity growth, or both.

Thinking about investing in Miami multifamily? I run pro formas on duplexes and triplexes every week. Schedule a free consultation , or follow @investmiami_livemiami on Instagram for daily Miami market intel.

Operational Tips That Actually Protect Your Cash Flow

Three small details that separate the deals that pencil from the deals that don't.

Check the utility meters before you offer

Walk the side of the building. Count electric meters. Count water meters. If each unit has its own meter, you can structure the lease so tenants pay all utilities directly . That moves $2,400–$4,800 a year per unit off your P&L. On a single-meter building, you're stuck eating utilities or trying to RUBS-bill — and tenants hate that. I've walked away from deals because of a single shared water meter.

Put every appliance on a service plan

An A/C compressor in Miami fails on a Sunday in August. The repair is $1,500 minimum. A fridge dies, $900. Stack four appliances across two units and you can spend $3,000–$5,000 in a bad year. A whole-property appliance and HVAC service plan ($40–$70/month per unit) caps that risk. It's not glamorous; it's just smart.

Self-manage two big units instead of hiring a PM for six

Two 3BR families, signed on 2-year leases, paying on the first of the month — you can run that on your phone. Six studios with constant turnover is a part-time job that you'll end up paying a manager to do. Bigger units = simpler ops = no PM fee = better cash flow. That's the operational argument for the unit-count rule.

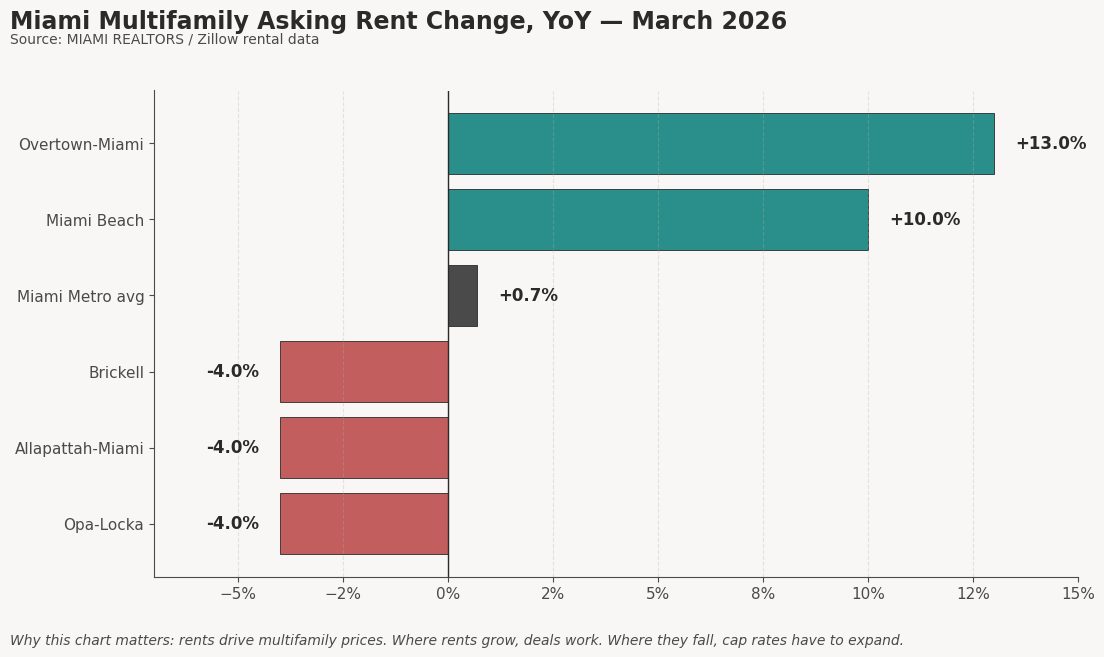

Rents Drive Multifamily Prices — It's a Numbers Game

Multifamily isn't a lifestyle purchase. It's priced off net operating income. So if you want to know where to buy, watch the rent.

Miami Metro just posted the highest multifamily rent growth in the entire South region — +0.7% YoY in March 2026 with 6.6% vacancy — per the MIAMI REALTORS April 2026 report . But the average hides everything. Overtown is up 13%. Miami Beach is up 10%. Meanwhile, Brickell and Allapattah are down 4%. That spread is where deals are made or lost.

When you're scouting a neighborhood, pull rent trends for the specific submarket. Don't trust "Miami is up" — Miami is a patchwork.

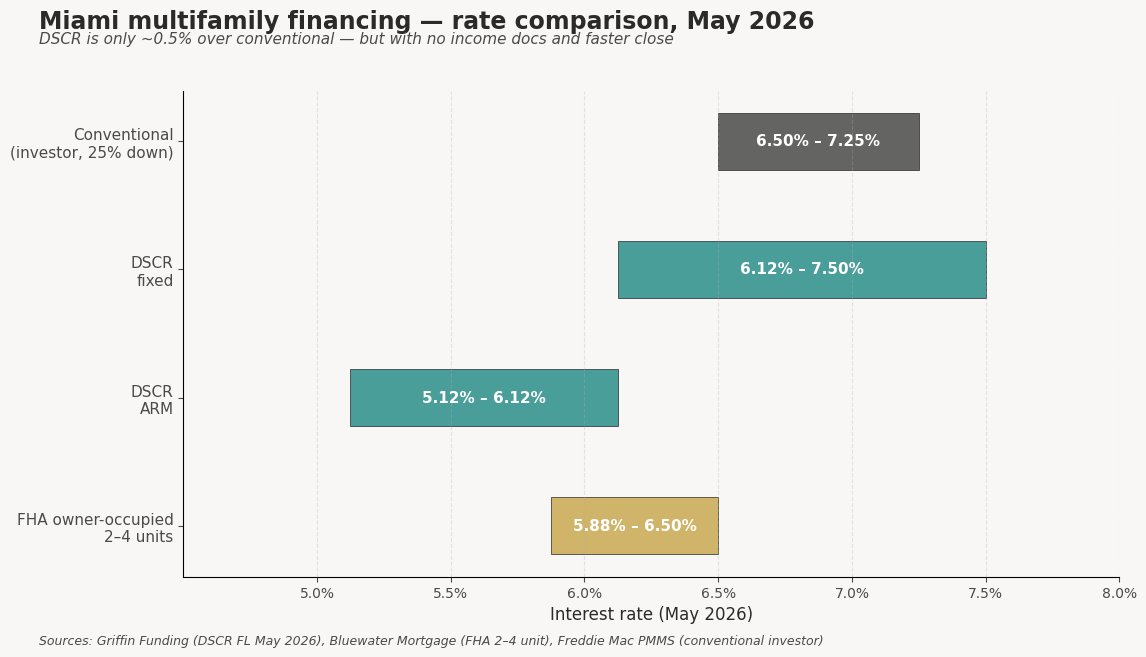

Financing Your First Miami Multifamily — Why 25% Down Wins

For a true investment-only property in Miami, I've found the cleanest deals pencil at 25% down with conventional financing . Here's why:

- 20% down works, but you carry PMI on most multifamily investor loans and your monthly payment eats into cash flow.

- 25% drops the rate by ~25–50 basis points, kills PMI, and the cash-on-cash math improves materially.

- 30%+ pushes cash flow higher but locks up capital you could deploy into the next deal.

If you can owner-occupy one unit for at least 12 months, an FHA loan on a 2–4 unit at 3.5% down is one of the best wealth-building plays in America. Live in one, rent the others, refinance out in 18–24 months. I've helped clients do exactly this in Coral Gables and Coconut Grove. Full investment property financing options on my main site.

DSCR loans — the small-investor tool I push hardest

If you're self-employed, have complex tax returns, or already own a few properties, a DSCR (Debt-Service Coverage Ratio) loan is the cleanest path I know. Underwriting is based on the property's cash flow, not your W-2 or tax returns. No income docs. Closes faster. Florida DSCR rates in May 2026 are running 6.125%–7.5% fixed and 5.125%–6.125% on ARMs — only slightly above conventional, with none of the documentation pain.

I have a short list of DSCR lenders I refer clients to — all of whom have closed Miami duplex and triplex deals in under 30 days. If you want an intro, reach out .

A 7-Step Roadmap to Your First Miami Multifamily

- Define the goal first — cash flow, equity, or both. This decides your zone.

- Get pre-approved — conventional or DSCR. Know your real budget before you tour.

- Pick 2–3 submarkets that match your zone. Pull rent comps for each.

- Tour 10+ properties before you offer. Walk the meters. Check the roof age. Look up the permit history.

- Underwrite every deal the same way — 25% down, 1.75% taxes, 0.3% insurance, 5% vacancy, current rates. Show the 5-year cash-on-cash and equity build.

- Inspect aggressively — roof, AC, panel, plumbing, termite, 4-point. Negotiate on findings, not feelings.

- Close, self-manage, and reinvest cash flow into the next down payment. That's how portfolios get built.

Want to see what your current Miami property is worth before you 1031 into multifamily? I run those numbers too. Or start at the top: buying a home in Miami .

FAQs — Investing in Miami Multifamily

How much money do I need to invest in multifamily in Miami?

For a typical small multifamily deal (2–4 units) priced between $650,000 and $1.2 million in 2026, plan on $175,000–$320,000 in total cash to close at 25% down — that covers down payment, closing costs (~3%), reserves, and a small make-ready budget. FHA owner-occupied drops that to $30,000–$50,000 if you live in one unit.

Is multifamily a good investment in Miami in 2026?

Yes — selectively. Miami Metro leads the entire South region in multifamily rent growth as of March 2026, vacancy is a healthy 6.6%, and new supply is slowing. But the market is a patchwork: Overtown rents are up 13% YoY while Brickell is down 4%. Submarket choice and unit-size discipline matter more than the macro headline.

What is the best neighborhood for multifamily investing in Miami?

There's no single best. For pure cash flow, parts of Allapattah, Little Haiti, and West Little River still pencil. For equity build, Coral Gables small multifamily and Coconut Grove duplexes outperform. For the middle path, look at Shenandoah, North Miami, and Westchester. I match clients to neighborhood based on risk tolerance, not the other way around.

Can I use a DSCR loan to buy a duplex in Miami?

Yes — DSCR loans work for 1–4 unit residential rentals, including Miami duplexes, triplexes, and fourplexes. Both units' rents count toward the DSCR calculation, which often makes a duplex easier to qualify than a single-family rental. Florida rates run 5.875%–7.5% as of May 2026.

How long does it take to close on a multifamily in Miami?

Conventional financing typically closes in 30–45 days from accepted contract. DSCR loans close faster — I've had clients close in 21–28 days when the lender, title company, and insurance binder all move quickly. FHA owner-occupied takes longest (45–60 days) because of the appraisal and underwriting overhead. Cash deals can close in under 14 days if title is clean. Build a 7-day inspection contingency and a 21-day financing contingency into your offer and you'll have negotiating leverage without putting your earnest money at risk.